Written by Janset An

Illustrated by Serena Fadil

King’s College Cambridge, Trinity College Dublin, Goldsmiths University, Swansea University, and University of Portsmouth are just a few universities across the UK that have made an explicit commitment to adopting a more ethical investment framework. Some have already divested from egregious corporate extractions of fossil fuels or violations of human rights through arms manufacturing.

The question, therefore, remains: why won’t LSE divest?

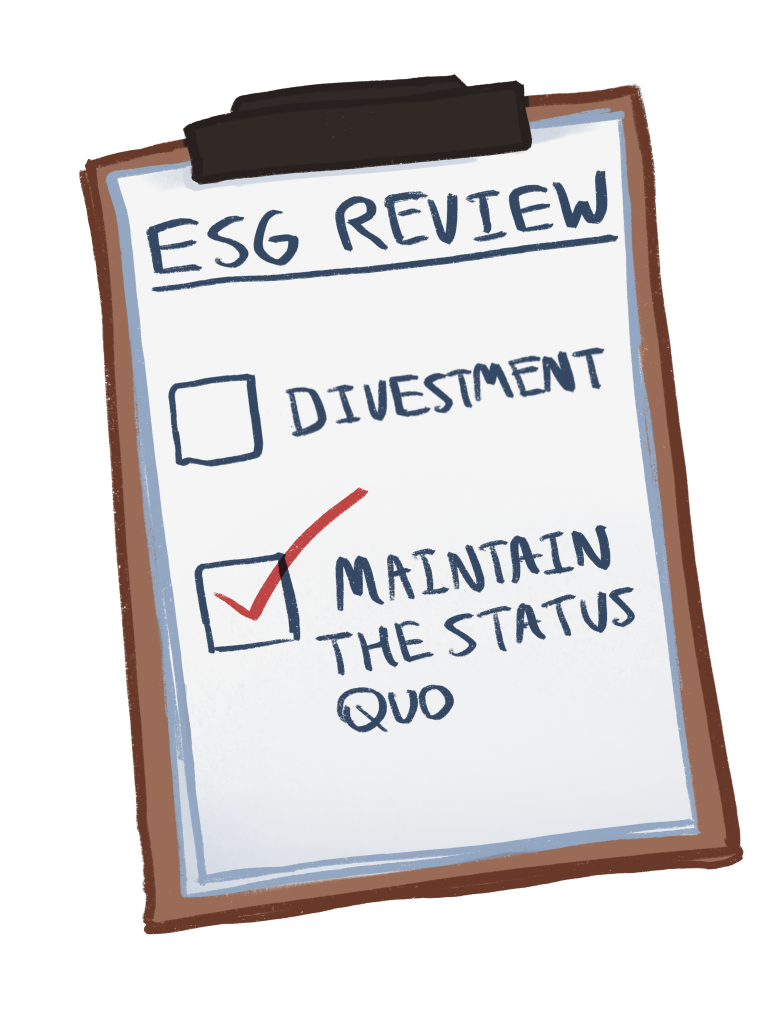

Some may argue there is no point in asking it anymore, as this question has already been deliberated upon. After all, an ESG (Environmental, Social, Governance) Review Process was announced in July 2024 to revisit LSE’s ESG Policy, which aims to minimise investment exposure to harmful industries.

Two bodies were created for this process: the Consultative Group and the Review Group. The former was composed of students, academic staff, and professional services staff, while the latter was independent members and academic experts of LSE. Through public workshops and welcoming online submissions, the school sought to engage and educate on the complexities surrounding nebulous institutional endowments.

In July 2025, the Council announced, following consideration of the Review Group’s report, that no Drastic changes in investment trajectories would take place. Therefore, the divestment dilemma seems to have been hashed out, and it is time to move on.

However, I believe we need to nitpick the ESG Review Process. Council’s decision to protect its portfolios was not because deliberation suggested it was the most commendable choice. Rather, divestment was ruled out ipso facto by the university —- in other words, it was never on the negotiation table.

Troublesome beginnings

Clear-cut responsibilities of the bodies involved, resourcing and financing were requirements for a streamlined investment policy review.

However, speaking to Dr. Dena Quaddimi, who was an LSE fellow in the Sociology Department and a member of the Consultative Group, I was informed this was not the case. She indicated that the whole process was strewn together with such haste that there was a lack of clarity and structure to the proceedings.

No meetings were held between the two groups in the preparatory stages of the process to clarify how discussions would materialise into actionable outcomes. Dr. Qaddumi noted that the ESG Review Process lacked some basic administrative procedures. The Review Group, which was responsible for organising meetings, kept no meeting minutes or set agendas in advance. The irony is that such a standard of conduct would not be tolerated even in the most trivial of student society meetings.

Furthermore, obscurity was exacerbated by the fact that the two groups only held four official meetings lasting 30 minutes to an hour over a five-month period. The last meeting between the two groups took place on 14 May 2025; however, this was unbeknownst to the Consultative Group. In fact, they found out at the start of this meeting that this would be their last point of in-person contact with the Review Group.

An Ignored Advisor

As outlined by the Terms of Reference, the role of the Consultative Group was to “advise” the Review Group in its analysis of the School’s ESG Policy. In retrospect, one can conclude that this onus was shrouded in great vagueness, as the Consultative Group’s opportunities to “advise” were restricted and, at times, blatantly rejected by the Review Group.

An LSE spokesperson has informed the Beaver that the boundaries of advice allegedly “followed the terms of reference.”

However, during the whole process, the Consultative Group received only one piece of documentation to offer up its comments on: the Review Group’s six-page rejection of the Consultative Group’s Working Paper 1.

Despite this, the Consultative Group took the initiative to make numerous suggestions and introduce nuance into discussions. Early on in the ESG Review Process, they requested to meet with LSE’s asset managers to discuss simulations of how finances would stand in the face of exclusionary criteria; they also urged the LSE to liaise with an external independent ethical investment advisor. However, both pieces of “advice” were ignored.

In fact, the Review Group rejected the former proposal, claiming that there was sufficient financial expertise already present in the Review Group. They also explained that financial simulations would be too costly — both reasons come across as patronising and unengaging.

Despite the Consultative Group’s multiple suggestions of action, none were taken up by the Review Group. Why?

Contradictions

It is one thing to reject a proposal after exhaustively discussing its implications, and it’s another to block the space before discussions even take place. It is unequivocal that the Review Group’s reluctance to adopt the Consultative Group’s suggestions was motivated by an aversion to potential financial losses. They argued that funds for education, research and scholarships would suffer if divestment were enacted. However, this logic exposes the entrenched oxymoron present in the university.

Firstly, investing in unethical activities is not the only profitable avenue- LSE could have looked into investing in net-zero real estate and low-emissions technology. With this current fiscal trajectory, the university is actively subverting its own policies, such as LSE’s Ethics Code and the Sustainability Strategic Plan.

Funding investments with positive externalities means that the LSE would be aligning its practices with the conduct they enthusiastically publicly claim to be committed to. As it stands now, the university is excellent at advertising itself, but its investments give it no basis to do so.

Secondly, there is something harrowing about how a global pioneer in social sciences research, like LSE, is knowingly funding arms manufacturers. The LSE claims it is committed to growing research into resolving geopolitical conflict through diplomacy and fostering the next generation of diplomats. Yet, part of LSE’s funds that support this invaluable research is being funded by an industry that thrives on the premise and encouragement of violent conflict.

LSE currently has over £70 million in 103 holdings in 113 companies involved in the global arms trade. It is easy to simply read a statistic, but conceptualising it with the full weight of its staggering implications is something that requires further elaboration.

For a six-month period in 2024, more tons of bombs were dropped onto Gaza compared to the combined effects of the bombing of Dresden, Hamburg and London in World War 2. One company LSE’s investment portfolio can be traced back to is Lockheed Martin, a supplier of F-35 Jets to the Israel Air Force. The thought that our university may have contributed to the financial stamp of approval on some of the jets carrying out these decimating missions on Gaza is spine-chilling.

Disappointing Outcome

LSE stands alone with its lack of engagement in overviewing its endowments. Dr. Qaddumi noted how colleagues in other universities participating in similar ESG Reviews had experienced an organised proceeding, with suggestions by staff being taken on board proactively by senior management.

LSE had the capability of resourcing and financing the ESG Review Process sufficiently; it has demonstrated this elsewhere on campus. When it comes to fostering a sense of belonging and enabling dialogues between different groups on campus, the LSE was not frugal at all — as part of the Innovation Fund for Campus Relations Group, the university funded eight projects.

Yet, they deemed financial simulations of different investment strategies too costly. They did not consider hiring an external independent ethics advisor. The hypocrisy is comical and striking proof of the university stigmatising and trivialising divestment.

Dr. Qaddumi shared her observations on how the Review Group’s approach to managing the university’s endowments seemed more akin to managing a for-profit business rather than a charity advancing higher education for the public benefit. If we adopt this metric of “business,” then we can certainly claim that the LSE has triumphed. Between 2023–2024, the Assets in Apartheid report revealed that LSE held £89 million in investments linked to alleged crimes against the Palestinian people, the global arms trade, and climate breakdown. By 2024–2025, that figure had risen to more than £131 million.

Ultimately, the ESG Review Process was a performative attempt by the university to give the impression that the student mobilisation around divestment had materialised into some tangible change. While handing out breadcrumbs of “higher degree of transparency” as a supposed legitimate outcome of the ESG Review Process, the institution was clearly working overtime in entrenching its economic ties to reprehensible corporations around the world.

An LSE spokesperson has contested however that the university will continue to “review the current investment filters related to fossil fuels, tobacco and armaments” to reduce appropriate exposure to these industries. They further add that the ESG Policy will be reviewed every five years “as is the general practice at peer institutions.”

Fundamentally, the handling of the ESG Review Process was a blatant disrespect to the work of the volunteers who contributed to the Consultative Group. According to the Terms of Reference, written submissions from the Consultative Group were not a requirement. Regardless, they engaged in exhaustive and meticulous research to produce a 20-page Concluding Report with 96 pages of Appendices. This Report did not even feature under the Council’s email sent as a school-wide announcement on the 10th of July- yet Council was considerate enough to include a link to the Review Group’s report. It took the Consultative Group reaching out to the School for their work to be rightfully circulated across campus.

Concluding Remarks

What I have covered in this article is only the tip of the iceberg.

“Why Won’t LSE Divest?” is going to be a series in which I seek to ensure not a single dubious stone is left unturned in the midst of a myriad of accounts, statements, and reports. We need to understand what happened in the 2024/2025 academic year to ensure we are better equipped with the language to call out questionable institutional conduct should it reappear again in the future.

In the second part of the series, I will analyse the composition of the Review Group and how their restrictive “positivist” mindset acted as an impediment to divestment ever being considered. I will show how what happened in 2025 was a continuation of avoiding ethical responsibility in investments as part of a trend that began a decade earlier in 2015.

An LSE Spokesperson said:

“Following the recent review of the Environmental, Social and Governance (ESG) Policy, LSE remains fully committed to strengthening our approach to responsible investment.

“The Review Group was comprised of experts from across the School to oversee the process and make recommendations to Council. To further facilitate the work of the Review Group, a separate Consultative Group was created, consisting of nine members of the LSE community (both staff and students) to provide insight and feedback across the year. The Consultative Group was formed through a rigorous process to ensure representation from across LSE and guarantee there were clear procedures in place around their roles and responsibilities. Extensive information about both group’s roles, responsibilities and activities can be found on the LSE website.

“The review itself included a thorough assessment of the policy and addressed questions raised by LSE students and staff related to the School’s investments.

“As a result of this project, beginning this academic year, LSE will review the current investment filters related to fossil fuels, tobacco and armaments to further reduce our exposure to these sectors, as appropriate.

“LSE Council will maintain the current approach to review the ESG policy every five years, as is the general practice at peer institutions. However, this is on the expectation that those overseeing the School’s investments may adapt or adjust these in between formal reviews as a result of input from additional mechanisms for transparency – such as annual general meetings which provide regular opportunity for the LSE community to share research related to investment; and other measures.”

Background information

There are several points in the article, we would challenge:

- In July 2025, the Council announced, following consideration of the Review Group’s report, that no drastic changes in investment trajectories would take place.

This is incorrect. Council examined reports of both the Review and Consultative groups, alongside other materials submitted in the review process, at its June 2025 meeting. The view of drastic changes is conjecture on the part of the writer and we explain the changes in our quote.

- The Review Group, which was responsible for organising meetings, kept no meeting minutes, nor set agendas in advance.

Although the Review Group did not keep standardised minutes, informal notes were kept and shared via email. We are not aware of any standardised minutes being kept by the Consultative group.

- The Consultative Group’s opportunities to “advise” were restricted and, at times, blatantly rejected by the Review Group.

We would challenge this. The boundaries of advice followed the terms of reference.